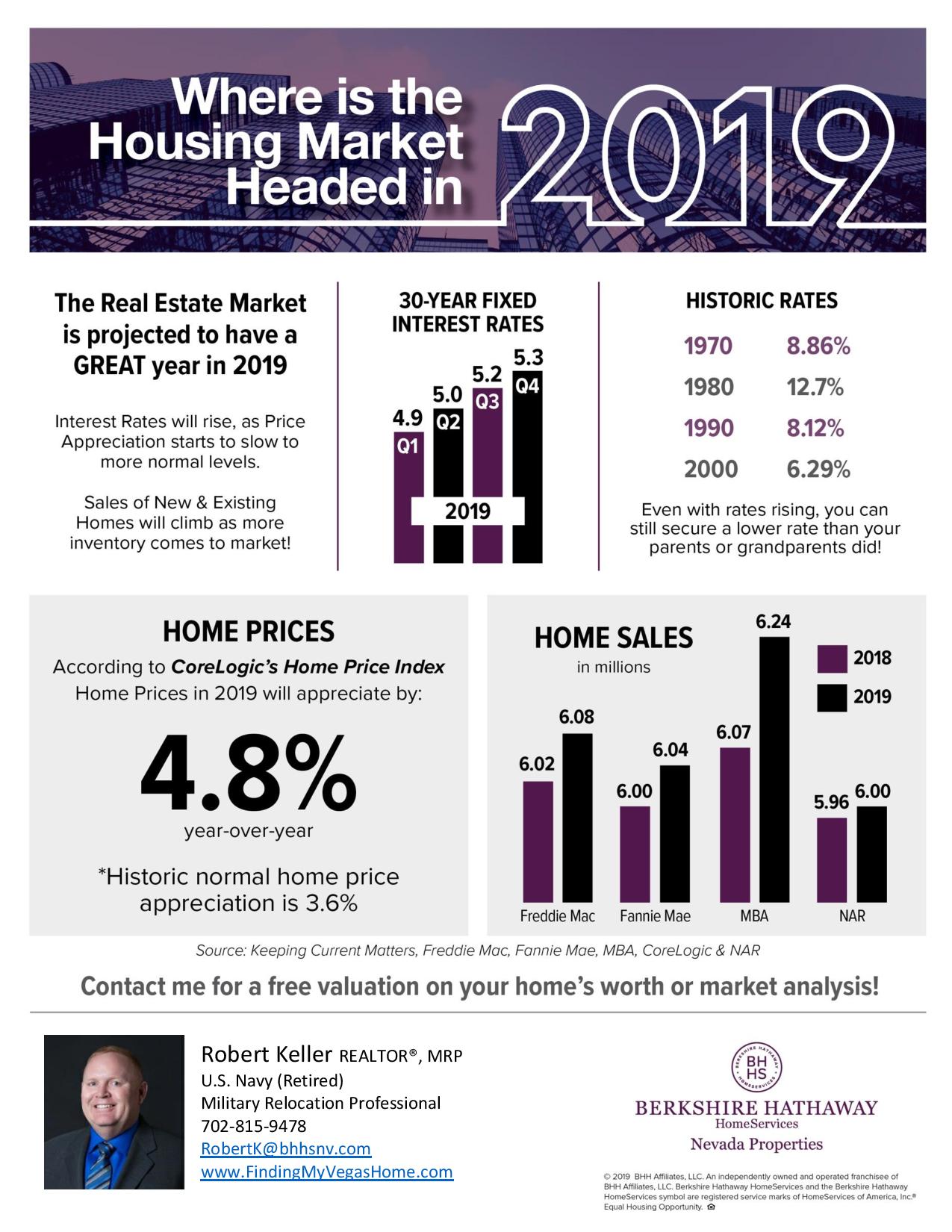

Where is the Market Heading in 2019? Check out the expected statistics in the infographic. If you’re looking to buy or sell a home in 2019 call/text me at 702-815-9478 to discuss the market and find a path to reach your goals.

Where is the Market Heading in 2019? Check out the expected statistics in the infographic. If you’re looking to buy or sell a home in 2019 call/text me at 702-815-9478 to discuss the market and find a path to reach your goals.

Step-by-Step Guide to Obtaining Your VA Loan Benefit

There’s a lot that is less than fantastic about military life. Missed birthdays and anniversaries. Worry during deployments. Picking up and moving time and again. But there are also perks to military life. One of those perks is the VA Loan Benefit. What’s not to like about a 0% down loan with no mandatory private mortgage insurance (PMI) and often with lower rates than a conventional loan? If you are eligible for this benefit, it’s one you should take advantage of.

Keep in mind: While it’s called a VA Loan Benefit, the VA does not provide home loans. What the VA does is act as the security of the loan, meaning the VA guarantees to cover the bank’s losses if there’s a default on the mortgage. This is added peace of mind for lenders!

Do you qualify? Did you or your spouse serve on active duty during wartime for 90 consecutive days? Or serve on active duty during peacetime for 181 days? Or serve in the National Guard or Reserves for six years? Were you or your spouse discharged from the service under honorable conditions? Or are you the spouse of a service member who died in the line of duty or as a result of a service-related injury or disability? If you can respond with “yes” to one or more of these requirements, you should be eligible.

Prove you’re eligible. You’ll need to obtain a Certificate of Eligibility (COE) to establish that you are indeed eligible for a VA Loan. You can do this yourself by completing a Certificate of Eligibility Request Form (VA Form 261880). Sign onto ebenefits.va.gov with your CAC card (ID card) to complete this form. This part of the process will require you to create an eBenefits account if you don’t already have one, or to login with existing credentials. Once on the site, click on the link entitled “Certificate of Eligibility for a Home Loan” and follow the instructions. Make sure to print out at least two copies of the COE—one for your own records and one for your mortgage lender.

Any questions or technical issues? You can contact VA/DoD at 1-800-983-0937. You can also ask your lender for assistance with obtaining your COE.

Speaking of lenders… While most lenders can offer VA Loans, it is to your advantage to choose a lender who specializes in them. One of the advantages of working with a military-serving real estate agent is that he or she knows and works with lenders with experience and expertise navigating the VA Loan program. This means smoother sailing for you!

Get your other documentation in order. You’re no stranger to needing documentation. Here’s where you’ll want to ensure you’re tracking which documents you’ll need: A DD-214 will verify an honorable discharge. You will also need to demonstrate that you have steady income sufficient to cover your mortgage payment and monthly expenses, so you’ll want to make sure you have your pay stubs or other proof of income readily available. While individual lender requirements may vary, you will likely be asked to produce bank statements, tax returns, W-2s, and orders (if you’re PCSing). Your lender will communicate any additional documentation that is necessary.

Pro tip: Put this information aside before you’re packing up if you’re in the middle of a move.

Once you’ve obtained your Certificate of Eligibility, put together your documentation, and assembled your dream team—an agent who is a pro at working with military families and a lender who’s comfortable with VA Loans—you’re ready to move forward with your home purchase. And in the process, you’ll be able to reap the financial rewards of a hard-earned benefit.

Available technology makes it easier than ever for military families to learn about their duty station. But searching on Google alone won’t cut it. That’s where social media swoops in to save the day and can make you an expert on your new neighborhood before you even get there!

Hack 1—Pinterest

I’m sure I don’t need to tell you how awesome Pinterest is for gathering and storing information in one place, but it is also a great tool for moving that shouldn’t be overlooked. As soon as you get orders to your next duty station, create a board on Pinterest titled with the name of your new duty station. Then start gathering pins related to the base and the area.

The best part about this? Many other military spouses have already traveled down the road you’re on. So it’s likely they’ve created or shared pins related to your duty station already. What’s better than collecting information curated by someone who’s been in your shoes?

Hack 2—Hashtags

Hashtags are a great way to geotag photos without actually using your GPS or “checking in” anywhere. Any time someone posts a picture to Instagram and adds a hashtag with a location that will be searchable by you (depending on their privacy settings).

So to start getting a visual idea of what your base and the surrounding areas look like, you can go on Instagram and start searching hashtags. Start by searching “#YourDutyStationName” (as in #FortHood). This will show you what real people are doing in the area and what they think about it.

A word of warning though: Take the comments and captions with a grain of salt. Everyone has a unique outlook on life so their comments might not be very objective.

Hack 3—Facebook Pages

I’m guessing that any time you receive orders, you immediately hop on Facebook and join the local spouse page at your new base. While there’s nothing wrong with that, there’s so much more to Facebook pages than just the spouses’ groups!

Hack 4—Snapchat

This one may sound a little goofy since Snapchat is used for more personal purposes (like sending funny photos of your face switched with your cat’s to your best friend). But it can also be used to help you discover more about your next base.

Hack 5—Facebook Live

Facebook Live is a fantastic tool for checking out a potential property. You can reach out to a friend and ask them to create a Facebook live video for you. They can set their audience for the video to just you so you’re the only one who can view the video.

They can then create a video while walking through a potential property. They can talk about what they like, don’t like, or anything that stands out. The best part about this tool is, once they’re done filming, they can save the video to their timeline (where only you will be able to see it!), and you can go back and review the video over and over again.

This makes it easier than doing a Facetime video with a friend and frantically trying to take notes while also trying to watch everything they’re showing you. This also helps you avoid the Facetime/video call barrier if you have phones that aren’t compatible.

Researching your next duty station doesn’t have to be all work… it can also be fun! By using the five tools above, you’ll get a fuller sense of what your next installation looks like and what life will be like on your next adventure!

How to Buy Your Not-Forever Home

Ahhh, your forever home. You know, the one you dream about when you close your eyes at night. The one with the backyard big enough to BBQ and the perfect spot for a vegetable garden. It’s close enough to your family but not too close. A magical, mythical place where you can paint the walls whatever darn color you want and use nails instead of Fun Tak to hang your family photos.

You likely already know exactly what you’re looking for in a forever home. But if your home address still varies dependent upon the whims of the military, you’re not working on a forever home schedule right now. You’re interested in buying your not-forever home. And that’s a whole separate animal. Here’s what you should keep in mind:

Figure out your non negotiables. ?If you have children, maybe a great school district tops your list of priorities. Perhaps you’re worried about the commute time for your significant other or the proximity to post. Maybe Spot is your world and a yard with a fence is a requirement for you. What are the things that aren’t up for debate? Once you’ve determined what those things are, be prepared to be more fluid and flexible with the other items on your “would-be-nice” list. Compromise on your forever home? Of course not. On your not-forever home? Absolutely, especially if your goal is to have the best possible financial outcome both as a new homeowner and as a future landlord.

It’s not just about you.? Okay, it is about you, but not entirely. Yes, this prospective not-forever home should be able to accommodate you comfortably now. Yes, in a kind world it should be a happy and welcoming place for you. Yes, it should put you in a good financial position where you’re not paying two mortgages concurrently.

But your not-forever home should be attractive to your future tenants as well. Your one-of-a-kind taste in wallpaper or funky bathroom tiling is, well, one of a kind. Keep in mind that you’re going to need other people to like what they see, too, or you’re going to struggle to keep the home rented out when you’ve already moved on to your next duty station. This reality means that you either need to consider purchasing a home that’s generally appealing rather than quirky. Or you need to be prepared to make it more attractive at your expense before renting it out—and toss those numbers into your financial math.

Do your homework.? Research what the property values are where you’re looking to purchase a home. How long do houses typically stay on the market there? How close to asking price do sellers usually get? Are home rentals common in the area? If you’re looking off post, is the area one where military folks are known to rent or own? The information you gather will tell you whether the home is a good fit for you now. But it will also give you a sense of how easy it will be to rent or sell your home when you’re moving on to your next location.

Remember that a great realtor can make a world of difference. ?You want someone who will be a fierce advocate for you. Someone who knows the area; is clear on your budget, needs, and non-negotiables; and is prepared to walk through fire to get the deal done for you. Such a person is worth every penny, both financially and for the “emotional savings” you’ll earn by having a highly competent professional on your team.

Until it’s time for the forever home, here’s wishing you luck in finding a perfectly adequate not-forever home. May it provide you warmth and security and wonderful memories. And when it’s served that purpose, may it quickly be grabbed up by the perfect future tenants who will protect your financial health.

66,100,000. That’s how many blogs, articles, resources, and opinions Google generously spits back when we type in “military families own or rent.” Obviously, renting versus owning a home is a quandary that’s very much on the minds of lots of folks. In the name of convenience (we don’t imagine you’ve got time to read over 60 million citations), we thought we’d highlight the key factors you should keep in mind if this is a decision that you too are currently looking at having to make.

Just to manage your expectations, we don’t have the “right” answer for you. There are too many variables that are unique to you and your specific circumstances to take into account. But we’ve got some great questions we hope will guide you to making the “right-for-you” decision.

What is your current housing situation?? Considering whether to rent or to buy is one thing if it’s your first home or apartment. That conversation quickly changes if you’re already responsible for an existing rental agreement or mortgage. For instance, if you’re living with family and searching for a place to call your own, you’re looking at potential numbers. If you’ve signed a year-long rental agreement or already hold a mortgage and are looking at another place, then you have two sets of numbers that need to play nicely together.

How is your financial health?? You need to have a very clear picture of where you stand financially before you think about committing future dollars. You don’t know what you’ll be able to afford if you haven’t yet been really honest with yourself about your current financial situation. If your present financial outlook is grimmer than you’d like, then are there other priorities like reducing debt or restoring a credit score that should take priority over home ownership?

Have you run the numbers for both renting and purchasing a home? Do you have a financial advisor who can review those numbers with you and take into consideration things like tax brackets, tax breaks, real estate appreciation, and such?

How important to you is that VA loan? If you use this benefit and then need to relocate elsewhere, you’ll need to have paid off your VA loan in order to be eligible for another. That means you can’t count on the help of a VA loan for the second property purchased.

Do you have a financial safety net? Are you prepared financially (and emotionally) to pay two mortgages or a mortgage and rent if you’re unable to sell your home before you need to move?

What is your future game plan? ?We’ll give you a moment to stop laughing. You could randomly sample any one thousand strangers on the street and they’d no doubt be as knowledgeable about what the military has planned for you as you are. You may not know where you’ll be in the next six months (we so wish that was an exaggeration). We get it. But what’s your plan for the plan? Are you early in your military career? How many years of PCSing do you anticipate having in front of you? How close—or far—is retirement for your military family? And what’s your plan for when retirement does come? Are you sipping margaritas from an RV that you use to hop from one child’s house to the other? Are you settling into a forever home? Your end game matters…or at least your next-several-years’ game does.

What about the “you” variable that folks forget to consider? ?How risk-averse are you? Are you reasonably comfortable with the uncertainty of the housing market? Are you willing to be geographically separated if the sale of a home requires one person to remain back while another proceeds to a new duty location? Are you open-minded about the idea of being a landlord if you find yourself needing to rent out a house that just won’t sell?

Do you like to shovel? Rake? Weed? Or do you have a teenage workforce to whom you can delegate such tasks? Are you handy or willing to shell out money when it comes to home repairs and maintenance? Do you like purple walls but not the twenty coats of primer necessary to cover them if you move out? (Purple walls won’t likely be your decision-making factor, but how you feel about decorating, renovating, and claiming a space as your own might be.)

Are you prone to collecting children, pets, or big boulders from all the places the military has sent you? How much space will you need? How challenging is it or might it be to find child-friendly/pet-friendly/boulder-friendly rentals in the area you’re considering?

The “right-for-you” choice is…? a series of conversations about your current situation, your financial health, your vision for your future, and your personal preferences and priorities. Nobody who tells you there is a singular right answer regarding whether you should rent or own is as invested in this outcome as you are. When all is said and done, this decision needs to be about what’s most important to you and your family.

5 Mistakes Military Homebuyers Make

And How to Prevent Them From Happening

Too often, military families feel like homeownership is out of reach. Maybe they’ve heard of friends being upside-down on a house in a bad market, desperate to sell. Or perhaps they struggle to find and keep renters in their home once they move away. Because of horror stories like this, many military families choose to be long-term renters until they can put down permanent roots.

Because military families often have compressed timelines and additional stresses to consider when buying a home, such as an unfamiliar city or upcoming deployments, they are at additional risk of making critical errors early on in the process. Fortunately for prospective military home-buyers, these worst-case scenarios are preventable, and home ownership can be a personally and financially rewarding experience if approached properly. Here are the top five mistakes to look out for if you are a military family considering a home purchase and, more importantly, how to avoid them!

Mistake No. 1 — Starting the Process Too Late

While some people are apt to wait until they arrive at their new installation to start house hunting, this rarely works out well.

On average it takes between 30 and 40 days to close on a home. But the military only offers you ten days of “free” temporary lodging. That means you have to account for 20-plus days of out-of-pocket living expenses. That can get expensive, stressful, crowded, and frustrating in a hurry.

Solution: As soon as you have an inkling you’ll be PCS’ing, start looking for a new home. Once the official orders arrive, you’ll be able to begin the process of buying or renting a home. That way, when you finally arrive at your new base after spending 50 hours driving across the country, you can skip temporary lodging and move straight into your new place.

Mistake No. 2 — Buying a House When You’re Not Financially Ready

The VA Loan is a benefit that makes homeownership a real possibility for many military families. But buying a house means you’re also buying into a lot more responsibility.

Air conditioning units break and water heaters tend to explode. Natural disasters CAN happen to anyone, and kids sometimes hit baseballs through windows. That’s life. And it’s pretty expensive sometimes. Putting all those home expenses on credit probably isn’t the best choice. And then the military will ask you to move once again, and you could suddenly find yourselves paying a mortgage on two homes because your old one hasn’t sold yet.

Solution: Before you buy a home, make sure you have a robust emergency/rainy day fund built up. That financial cushion will allow your family to take care of home emergencies without your finances spiraling out of control.

Mistake No. 3 — Not Buying a House for the Long Game

This is probably the biggest mistake military home buyers make. Homes appreciate (gain value), but it takes years to see the value increase. Location impacts this significantly. But buying a home with the expectation you’ll be able to sell it for a profit in just a couple years when you get new orders isn’t very realistic. If you’re selling after only a few years you’ll be lucky to break even, and you’ll be more likely to lose money on the transaction.

Solution: When buying a home, buy it with the long game in mind. That means being prepared to become a military landlord the next time you PCS. Selling too soon might result in the loss of thousands of dollars, whereas renting the property ensures that the mortgage is covered by tenants and you can continue to build equity. Military homeowners have to think beyond the two or three-year planning horizon that is typical for military families.

Mistake No. 4 — Buying in the Wrong Market or Neighborhood

You always hear real estate agents talking about “location, location, location!” There’s a good reason for that. A home that’s in a desirable neighborhood for your family doesn’t mean it’s desirable to everyone else.

You also have to consider the market. Are there enough people moving to and from the area to support you being able to rent or sell your home? Is the market over-saturated with homes, making yours just one of the thousands up for sale? Not enough demand can be bad, but too much supply can be worse.

Solution: When buying a home, think beyond your family and your circumstances. You might love living out in the country, but many other families might not want to live so far from the installation. A downtown loft might be ideal for your family, but too expensive and too cramped for many other families. Think about your potential buyers and renters before committing to a new place.

Mistake No. 5 — Buying the Wrong House

Yes, that is a thing. Just because you like a house, doesn’t mean other people will. When buying a home at your new installation, keep in mind that it’s not going to be your forever home. Even if you plan on coming back to it in the future, you need to have a plan for what you’re going to with it in the meantime.

Solution: When buying a home, think beyond your family and your circumstances. You might love having a split level home with only two bathrooms, but that could be an absolute deal breaker for many other families. Ask yourself, “What is desirable about this house to the general population? What is undesirable about it?” Considering what would be desirable to other families before committing to a house will help your chances of selling or renting out your home when it comes time for you to PCS again.

Conclusion

Buying a home while still serving in the military can be risky, but when done properly it comes with the reward of long-term financial stability. Do your homework, keep the potential hazards in mind, and find a savvy agent. So long as you avoid the common mistakes that military families sometimes make, you too can own your very own piece of the American Dream!

One of the biggest hurdles real estate agents face with connecting to the veteran and military population is a lack of understanding of the VA loan process.

In the next 5 minutes, you will learn about the Top 3 VA Loans Myths.

Myth 1: VA Loans Take Way Too Long To Close

Fact: VA Loans Close Just as Fast as Conventional Loans and Even Close More Frequently

There’s a lingering myth that loads of red tape cause VA Loans to close more slowly than conventional loans. This is simply not true.

According to national data collected by Ellie Mae, conventional loans closed in an average of 40 days while VA Loans closed in an average of 41 days.

Ken Robbins, Co-Founder of Millie, personally experienced this process just a few years ago. He was buying his current home with a VA loan as he was transitioning from the military. The home closed in just under 30 days.

Not only do VA Loans tend to close just as fast as conventional loans, but the Ellie Mae data also suggest that borrowers who take out VA Loans are actually more successful in closing than those who take out conventional loans. Typically, 68% of VA Loans closed while only 49% of conventional loans closed.

Myth 2: VA Loans are More Risky Than Conventional Loans

Fact: VA Loans Have Been The Safest On the Market Since The Housing Crash of ‘08

VA Loans’ competitive interest rates and $0 down payments often leave people thinking, “What’s the catch?” Many assume that VA Loans are more risky because they come with so many benefits. The fact of the matter is: VA Loans have had the lowest foreclosure rates of any type of mortgage for the last seven years, according to the National Delinquency Survey.

This is something we have seen SO many times. A realtor on the selling side will tell their client to turn down an offer from a buyer using a VA loan despite the offer being for MORE MONEY than the conventional loan buyer. Thus, they just cost their seller money. The amount of money for a down payment is not an indicator of the strength of the buyer in all cases.

Myth 3: The VA Appraisals Tend to Be Conservative and Undervalue Homes

Fact: All Appraisals Cause Differences of Opinion, and VA Appraisals Are No Different

VA appraisals have developed a bad reputation for undervaluing homes, but no data suggest that these appraisals over more conservative estimates than conventional appraisals. Rather, it seems as if difference of opinion about property value is just a common phenomenon that affects all types of loans.

A 2012 study from the National Association of Realtors showed that 1 in 3 real estate transactions had problems because of an appraisal.

The VA appraisal process, like all other appraisal processes, is influenced by subjective judgments and statistics from supposedly comparable homes that might not offer good market information.

In Ken’s experience, he rarely saw VA appraisals differ significantly from others. When he and his wife bought their home, the VA appraisal was ABOVE their purchase price, meaning they gained instant equity in the home.

The appraisal was done efficiently and they missed no closing deadlines as a result.

If you need an agent that understands the VA Loan Process and can help with your real estate needs please feel free to reach out to me at your convenience at 702-815-9478, or RobertK@bhhsnv.com

I Pledge to Serve Those Who Have Served

Every real estate agent has a responsibility to provide the best home buying experience and resources available to his or her clients. That’s why I’ve pledged to ask every client “Did You Serve?” As a Veteran, you are eligible for many benefits earned through your service, among them is the advantages of the VA Home Loan program. It’s my privilege to educate you on these home buying benefits and to help make those benefits accessible and attainable.